Is it worth going to a mortgage broker?

Can a mortgage broker still help you find the best deal – or are you better off going direct to the lender?

Whether you're buying your first home or simply looking to remortgage, you might be considering using a mortgage broker to find the right deal for you.

As new research suggests that mortgages are placing the biggest mental health strain on homeowners over anything else, we assess whether it’s still sensible to go it alone when it comes to getting the best deal or whether it’s time to consult the experts.

Mortgages have got us worried

Since the government's mini-budget in September 2022, mortgage rates have risen sharply. And, although there are some green shoots of hope as the housing market begins to stabilise and we are seeing more mortgage deals below 5% – there's no doubt about it: mortgages are more expensive now than they were in the first three quarters of 2022.

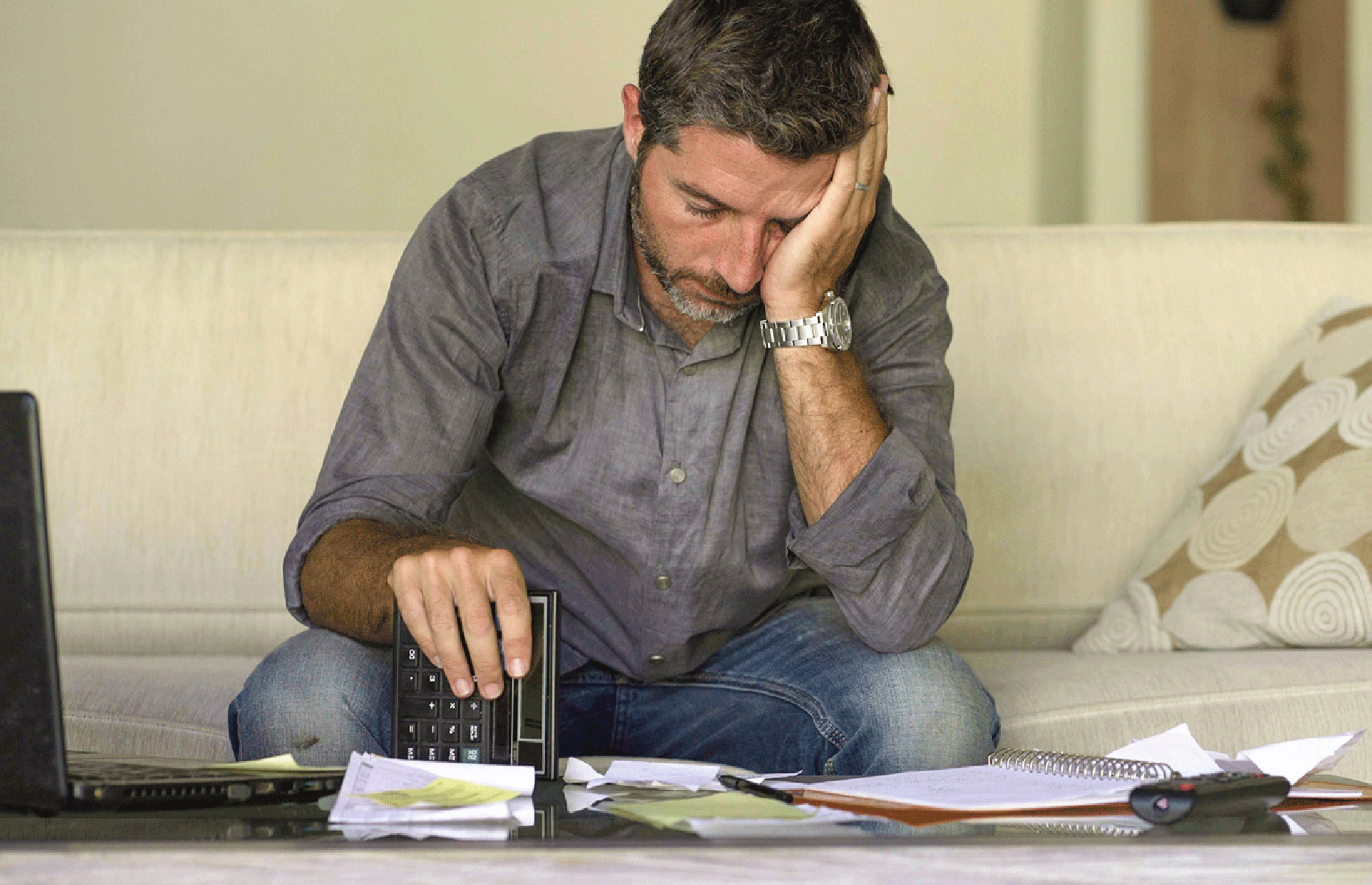

According to a new study by iPlace Global, homeowners and prospective buyers are woefully unprepared when it comes to looking for a mortgage and the pressure of it all is taking a toll on our wellbeing.

iPlace Global says that almost one in four (22%) of existing homeowners polled say that their mortgage has placed the biggest strain on their mental health. The same research suggests that one in five prospective homebuyers have no idea whether a fixed-rate mortgage or a variable mortgage is more cost-effective for them.

These findings come after separate research by financial software firm Dye & Durham found that 69% of people are worried about the financial future for themselves and their friends and family, with 30% of homeowners saying they were concerned they may have to miss a mortgage payment over the next year.

These alarming figures are not surprising given the current state of the housing and mortgage markets, says Simon Bath, CEO of iPlace Global, who points to a large number of mortgage deals coming to an end in 2023 – 1.4 million according to figures from the Office for National Statistics – as a reason for the concern.

Simon says: “Despite there being some positive news to come out of the mortgage market at the start of this year – with many lenders lowering their deals in light of waning demand – our data reflects that mortgages are one of the leading causes of stress for homeowners that are coming to the end of their deals."

With all this in mind, we look at the pros and cons of going the intermediary route and whether or not you should get a mortgage broker.

Image credit: 2019 TheVisualsYouNeed / Shutterstock

What does a mortgage broker do?

In short, a broker will look at your financial circumstances, tell you what mortgage deals are available to you and advise on which one makes the most financial sense. This is particularly useful when navigating the minefield of mortgage offers to find out which one works best for you.

For instance, iPlace Global has done some sums regarding what certain types of buyers can expect to pay on a mortgage given the current state of the market. Based on a typical property worth £287,880 and assuming a 15% deposit (£43,182) and a mortgage term of 25 years, it estimates that a family with an average monthly household income of £2,691 could spend almost 69% of their take-home pay each month on a two-year fixed rate mortgage.

Based on the same deal, a first-time buyer earning around £2,156 per month could expect to make repayments of an alarming 70% of their salary. These ratios come down slightly on a two-year variable rate but jump enormously on a standard variable rate. That's enough to keep anyone up at night!

How much does a mortgage broker cost?

According to Unbiased, you can expect to pay £400-£500 for a mortgage broker, but sometimes they charge nothing at all! If there is a fee – make sure you know what this is upfront and seek assurances that it is only paid if the mortgage goes through. Some brokers don't charge the customer and just take a commission from the lender, and some shrewd brokers receive both.

The case against brokers

Brokers have had a tough time over the last few years, and one of their biggest problems has been the fact that lenders often reserve their very best rates for borrowers who go direct, not through the broker channel.

The internet also has a role to play in driving people to go direct as the proliferation of online comparison sites has made it easier for potential borrowers to search the market. Try the loveMONEY mortgage tool to see which mortgage deals fit your circumstances.

You no longer need to spend an afternoon traipsing up and down the high street to pick up a stack of mortgage literature. Now you can type in your precise needs and a clever mortgage tool will find the most relevant products for you. Even better, you can see how much your monthly repayments would be and what the total cost, including fees, would be over a period of your choice.

Many borrowers feel that they simply don’t need a mortgage broker to help them sift through the market, now the internet does it for them. But are they right?

The case for brokers

Image credit: 2017 Ground Picture / Shutterstock

Firstly, to address the points above. Brokers may not be able to arrange direct-only mortgages for you, but they are free to tell you about them and, if they are the best deal for your specific needs, recommend you take one.

In other words, the fact that direct-only deals are some of the best on the market doesn’t necessarily mean you shouldn’t use a broker.

Secondly, while the internet does make it easier to compare deals, many comparison sites don’t compare all deals from all lenders, including those mortgages from broker-only lenders.

They also can’t give you a full explanation of the pros and cons of different deals, or take all of your circumstances into account. This leads us to the very real benefits of brokers:

Whole of market

A lender won’t tell you a competitor has a better deal. However, a mortgage broker scours the market to find the best deal for you from across a wide range of UK mortgage lenders.

Approved first time

One of the biggest frustrations for borrowers is applying for a mortgage only to be rejected by the lender, or be told that they will offer a lower sum than you need for the property of your dreams.

Lenders have very different lending criteria and a mortgage broker will be au fait with what all the major lenders will, and won’t, accept. This can save you time and can also mean the difference between your purchase going through or the chain falling apart because of unnecessary delays.

Doing the hard work

Dealing with a mortgage lender can be frustrating and time-consuming, particularly if you don’t have one point of contact.

A broker takes a lot of the hard work out of it by filling in forms, making phone calls and chasing the lender to get the deal through to completion. You can sit back and relax!

Looking out for you

Brokers look after your needs, as they want to keep you as a client. It’s in their interests to do the best job possible for you, from finding you the best mortgage and insurance deals from across the market to getting the deal through quickly.

Crucially, they are with you for the long term, so when they see a better deal come along in the future that would save you money, they will get in touch – something your mortgage lender is never ever going to do.

Broker or no broker, it pays to be mortgage savvy

Whether you choose to go down the mortgage broker route or not, you should make yourself aware of the different types of mortgages out there.

The biggest difference is between fixed-rate mortgages, which have a set interest rate for a specified period meaning that homeowners can make sure there are no nasty surprises should base rates change, while variable rates are dependent on current interest rates. While the initial rates for variable-rate mortgages are often lower, you do run the risk of your mortgage going up if interest rates rise. On the flip side, you will benefit if they drop.

Simon Bath says: "As many Brits come to the end of their fixed rate deals, some are questioning whether to switch to a variable deal or stick with the fixed package they currently have. For one of the most important purchases of your life, it's vital to arm yourself with the most up-to-date knowledge that's currently available."

Broker or no broker, Simon says it's crucial to be well informed: “Given the changing landscape within the mortgage market, prospective homebuyers must now – more than ever – take their time to compare services and providers to get the best deals possible when finding the home of their dreams."

How to find a good broker

Consumer rights champion, Which?, has some great advice on finding a trustworthy mortgage broker, from the key questions to ask to busting mortgage broker jargon.

Your home or property may be repossessed if you do not keep up repayments on your mortgage.

Comments

Be the first to comment

Do you want to comment on this article? You need to be signed in for this feature